When is a Cloud not a Cloud?

Further thoughts on yesterday’s post, prompted by some of the conversations about it

I realised that in yesterday’s post I implied that the key difference was between different markets; that in some markets, a full-on enterprise sales push is required, while in others you can rely on word of mouth to allow good products to emerge.

I do believe that there are macro divisions like that, but even within a more circumscribed group of products, you can still see big differences that are driven at least in part by sales activity.

Let's talk about cloud.

The conventional wisdom is that Amazon’s AWS dominates because of under-the-radar adoption by developers. In this view, teams who wish to move faster than corporate IT’s procurement and delivery cycles use their company credit cards to get resources directly from AWS and release their code directly to the cloud. By the time the suits realise this has happened, the developers have enough users on their side that it’s easier just to let them keep on doing what they’re doing.

There is a fair amount of truth to this story, and I have seen it play out more or less in this way many times. What is neglected in this simple scenario is the other cloud vendors. There was a while back there when it wasn’t obvious that AWS was going to be the big winner. Google Compute Engine seemed like a much better bet; developers already had a high comfort level with using Google services. In addition, AWS initially offered bare-metal systems, while GCE had a full-stack PaaS. Conventional wisdom was that developers would prefer the way a PaaS abstracts away all the messy details of the infrastructure.

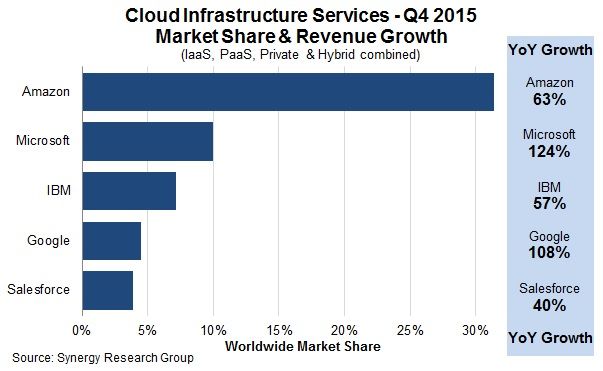

Of course it didn’t work out that way. Today GCE is an also-ran in this market, and even that only thanks to a pivot in its strategy. AWS dominates, but right behind them and growing fast we see Microsoft’s Azure.

Data from Synergy Research Group

And look who’s right behind Microsoft: IBM! Microsoft and IBM of course have huge traditional sales forces - but what some commentators seem to miss is that the bulk of AWS’ success is driven by its own big enterprise and channel sales force. A developer getting a dozen AMIs on the company AmEx might get usage off the ground, but it doesn’t drive much volume growth. Getting an enterprise contract for several thousand machines, plus a bunch of ancillary services? Now we’re talking.

Also note who’s missing from this list - anything driven by OpenStack. There are as many opinions on OpenStack technology as there are people working on it - which seems to be part of the problem. The one thing that seems clear is that it has not (yet?) achieved widespread adoption. I am seeing some interest on the SDN/NFV side, but most of those projects are still exploratory, so it remains to be seen how that market shakes out - especially with competition from commercial offerings from Cisco and VMware ramping up.

A good sales force won’t be able to push a terrible product, not least because sales people will jump ship in order to have a better product to sell, which makes their job easier. However, a good sales force can make the difference between a good product emerging from the churn, or not.

Underestimate sales at your peril.

Image by Jan Schulz via Unsplash